Filing Tax in Malaysia

A short guide for digital nomads, remote workers, freelancers, and founders with foreign companies. YA 2024, 2025, and 2026.

Ref: Malaysian Income Tax Act 1967 and relevant Public Rulings

Electra Frost at Network School • 4/4/2026

Before We Begin

General advice disclaimer

This presentation provides general information about individual tax filing under the Malaysian Income Tax Act 1967. It is not tax advice or a substitute for professional consultation specific to your circumstances.

Your obligations depend on your individual facts: how many days you spend in Malaysia, where you physically perform your work, and how your income is structured. The legislation and LHDN administrative practice referred to here may change.

Confirm your position with a qualified tax adviser before filing or deciding not to file.

Context

Who is this for?

You are a foreigner living in or spending time in Malaysia. Your income comes from outside Malaysia.

- You work remotely for a foreign employer or your own foreign company

- Your income is salary, directors' fees, or dividends drawn from that foreign entity

- You derive fees from overseas as a freelancer or independent contractor

- You have no Malaysian employer, no Malaysian clients, and no Malaysian business

- You may hold a DE Rantau visa, tourist visa, or other entry permit

Residency

Resident or non-resident?

Your tax residency is determined by physical presence, not citizenship or visa type.

The main test

Present in Malaysia for 182 days or more in a calendar year = resident for that year of assessment.

Other tests

Linked consecutive-day periods (s.7(1)(b)), the 90-day test across multiple years (s.7(1)(c)), and deemed residency (s.7(1)(d)) can also apply.

Below 182 days

If you don't pass any test, you are non-resident for that year. This is common for YA 2024 arrivals.

—— RESIDENCY

Record every entry & exit

Keep a spreadsheet logging every border crossing. This is your primary evidence for the 182-day test — and linking periods across years.

| Date |

Direction |

From / To |

Purpose |

Days in MY |

| 15 Jan 2026 |

Entry |

Singapore → Malaysia |

Return to NS base |

|

| 28 Feb 2026 |

Exit |

Malaysia → Thailand |

Holiday |

45 |

| 5 Mar 2026 |

Entry |

Thailand → Malaysia |

Return to NS base |

|

| 20 Jun 2026 |

Exit |

Malaysia → Australia |

Client meetings |

107 |

Why the purpose matters

The reason for travel can determine whether days abroad count toward linked residency periods under s.7(1)(b) and the 90-day test under s.7(1)(c). Record it while you remember it.

Tips

Both arrival and departure days count as full days. Back it up with passport stamps or immigration app screenshots. Keep one sheet per calendar year.

Residency

How the 182-day count works

The primary test is simple: are you physically present in Malaysia for 182 days or more in a calendar year?

Calendar year

The count runs 1 January to 31 December — not a rolling 12 months. Each year of assessment stands alone.

How to count

Both your day of arrival and day of departure count. Any part of a day physically present in Malaysia counts as a full day. Days do not need to be consecutive — every day physically present adds to your total.

If you’re based at NS

If Malaysia is your home base and you’re not away for extended periods, you will almost certainly pass the 182-day test without needing the other provisions.

But if your year is tight — maybe you spent two months in Europe over summer and did a long conference circuit in Q4 — then you may need the linking provisions on the next slide.

Residency

When years link & temporary absences

If you fall short of 182 days, two other tests can still make you resident. Both reward consistent presence and good records.

Linked periods — s.7(1)(b)

If you have a block of presence in Malaysia that connects to another block in the same or an adjacent year, temporary absences between them can be treated as days in Malaysia.

The absences must be connected to your Malaysian life. A conference in Singapore, a holiday in Thailand, visiting family abroad — these typically qualify. The legislation doesn’t define “connected” precisely, which is why recording your purpose of travel matters.

The 90-day historical test — s.7(1)(c)

This is the safety net. If you were present for at least 90 days this year, AND you were resident or present for 90+ days in three of the four preceding years, this year counts as resident.

Your history supports the current year — not the other way around. This is why keeping records going back at least five years matters.

You have a long-term home base in Malaysia but move around for work and conferences. Short trips abroad don’t break your residency — but your records need to show that Malaysia is where you return to and that your absences are temporary.

Scope of Tax

What are you taxed on?

Resident

Malaysian-sourced income, plus foreign-sourced income received in Malaysia (from 2022, subject to exemptions through 2036 if taxed at source).

Progressive rates: 0% to 30%

Eligible for reliefs, rebates, and DTA relief with 80+ treaty countries.

Non-Resident

Malaysian-sourced income only. Foreign-sourced income is not taxable regardless of where you receive it.

Flat rate: 30% on employment and business income.

No reliefs, no rebates, and no DTA relief available.

Source Rules

Where is your income sourced?

Malaysia taxes income where the work is physically performed. Not where you are paid. Not where your company is registered.

- Employment income: taxable if you do the work while physically in Malaysia

- Self-employment, consulting, freelancing: taxable if your services are performed while in Malaysia

- Dividends, interest, passive returns: foreign-sourced if arising abroad. Exempt for residents through end of 2026 (if taxed at source)

- Capital gains: not taxed in Malaysia except on Malaysian real property

"I'm paid into a foreign account, so it's not taxable." Wrong. Source depends on where you did the work.

Special Rules — Non-Residents

The 60-day exemption

For non-residents: employment income is exempt if you are in Malaysia for 60 days or fewer in the calendar year (PR 8/2011).

Lose it once you cross 60 days, even across multiple visits.

Freelancers, contractors, and directors' fees are excluded from this exemption. It applies to employment income only.

For most digital nomads and founders spending meaningful time in Malaysia, the 60-day exemption will not apply. The question then becomes whether a DTA can help.

Special Rules — Non-Residents

DTA relief: Article 15

If you are non-resident and tax resident in your home country, a DTA may override Malaysia's right to tax your employment income.

Step 1 — Domestic Law

Work performed in Malaysia is Malaysian-sourced under s.12 and s.13. Under domestic law, it is taxable at 30% flat.

Step 2 — DTA Override (s.132)

Article 15 can reallocate the taxing right to your home country if all three tests are met. This is not automatic. You must claim it in your return with a Certificate of Tax Residence from your home country.

1. Present ≤ 183 days in a 12-month period

2. Paid by or on behalf of a foreign employer

3. Salary not borne by a Malaysian entity (PE)

Fail any test → Malaysia taxes at 30%. Freelancers and contractors: Article 15 does not apply.

This is a non-resident mechanism. Residents cannot use Article 15 to avoid Malaysian tax on work done in Malaysia. Residents use bilateral tax credits (Schedule 7) and FSI exemptions instead.

Special Rules — Residents

FSI exemption and bilateral tax relief

Foreign-Source Income Exemption

Residents are temporarily exempt from tax on foreign-sourced income received in Malaysia (dividends, interest, royalties, rental, investment returns already taxed abroad). Runs through end of 2026, extended to 2036.

Does not cover income from services performed in Malaysia. That is Malaysian-sourced regardless of where paid.

Bilateral Tax Relief (Schedule 7)

If Malaysia taxes income already taxed overseas, you can claim a credit for foreign tax paid (up to the Malaysian equivalent). Must be a Malaysian tax resident.

Claim within 2 years of the relevant assessment year. If your foreign return is filed later, you can amend your Malaysian return to claim the credit with evidence of tax paid.

The Nil Filing Question

No Malaysian-source income. Do you file?

Section 77(1) of the ITA requires "every person chargeable to tax" to furnish a return.

No chargeable income means no strict filing obligation.

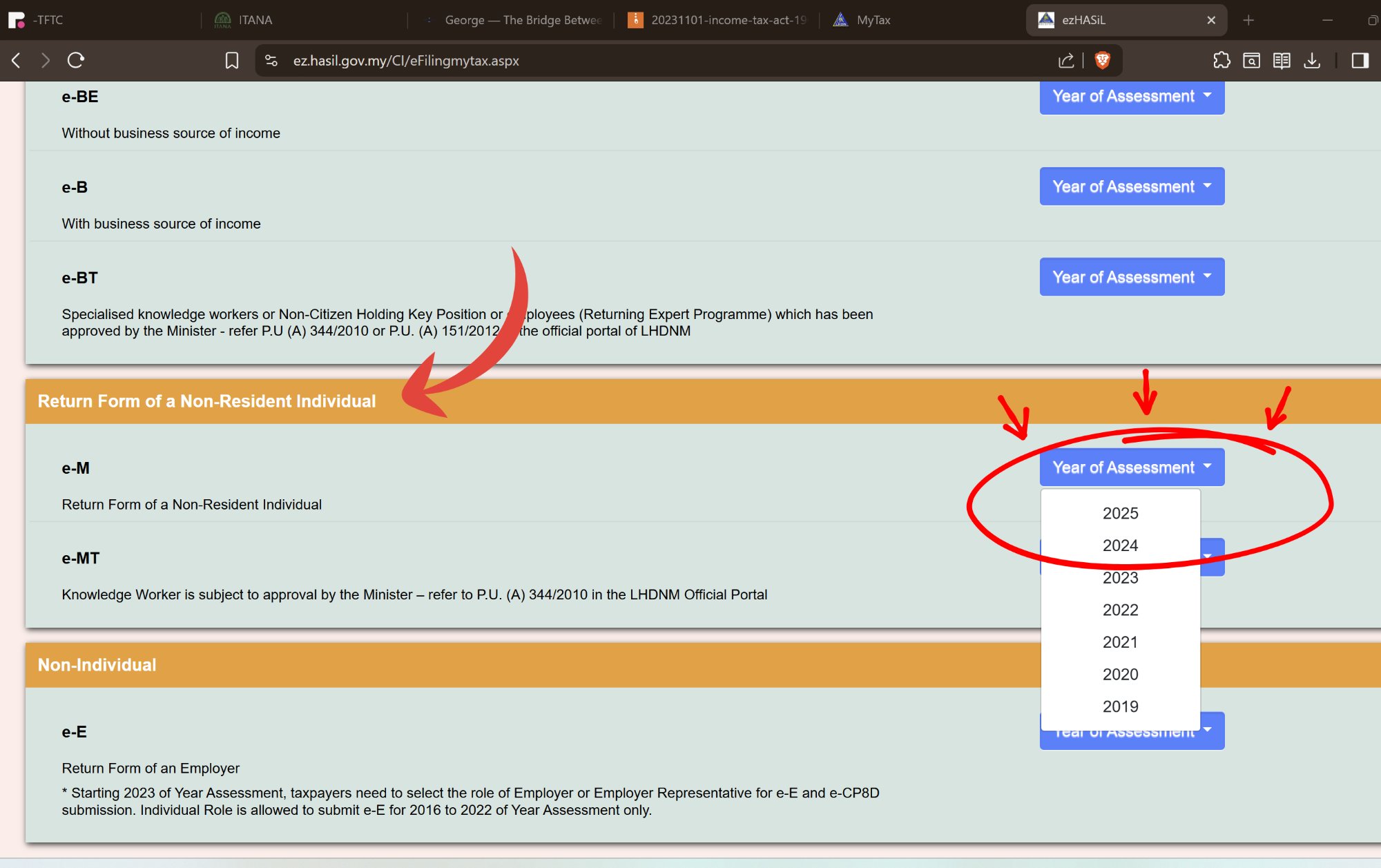

LHDN Non-Resident Guidance:

"If taxable, you are required to fill in M Form."

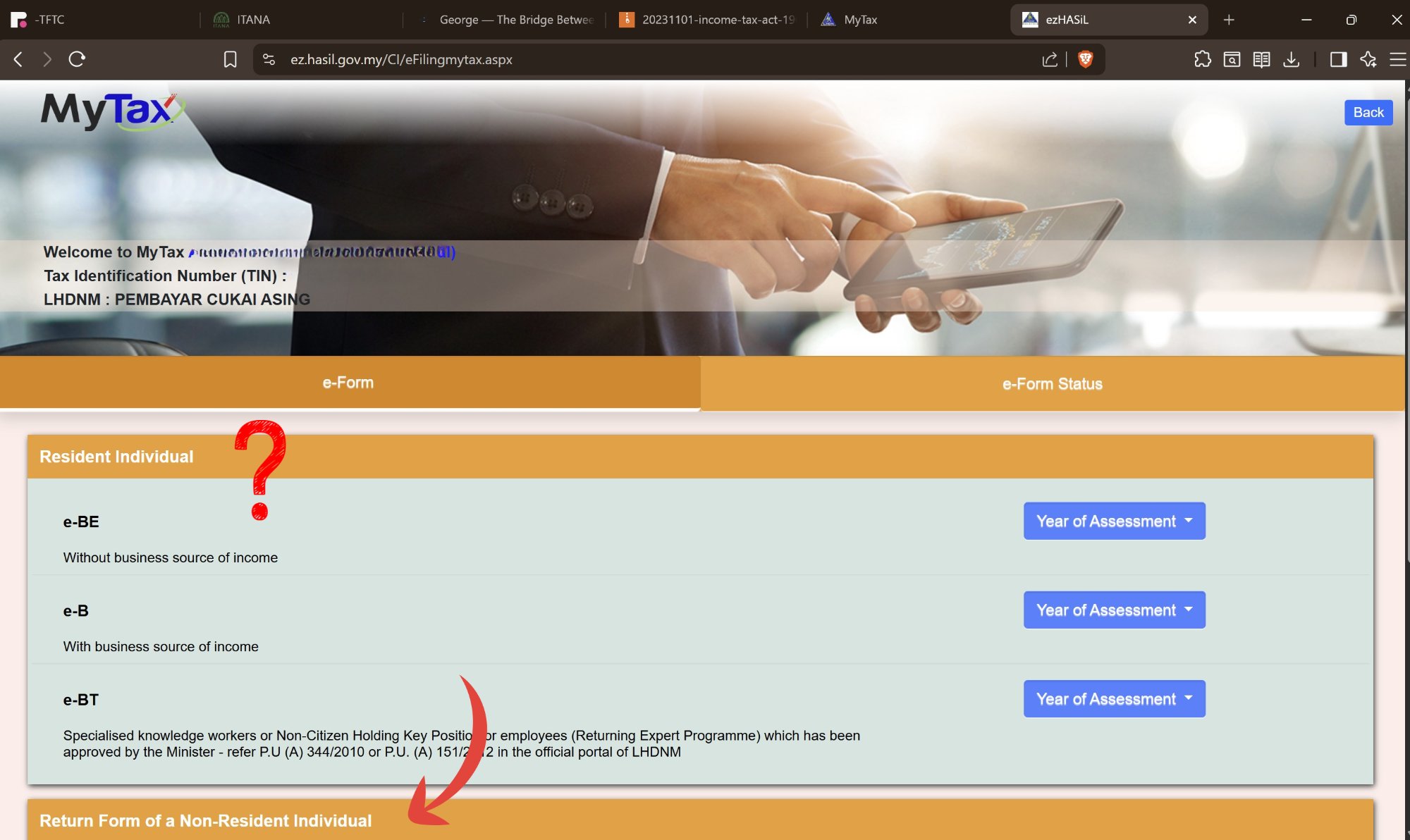

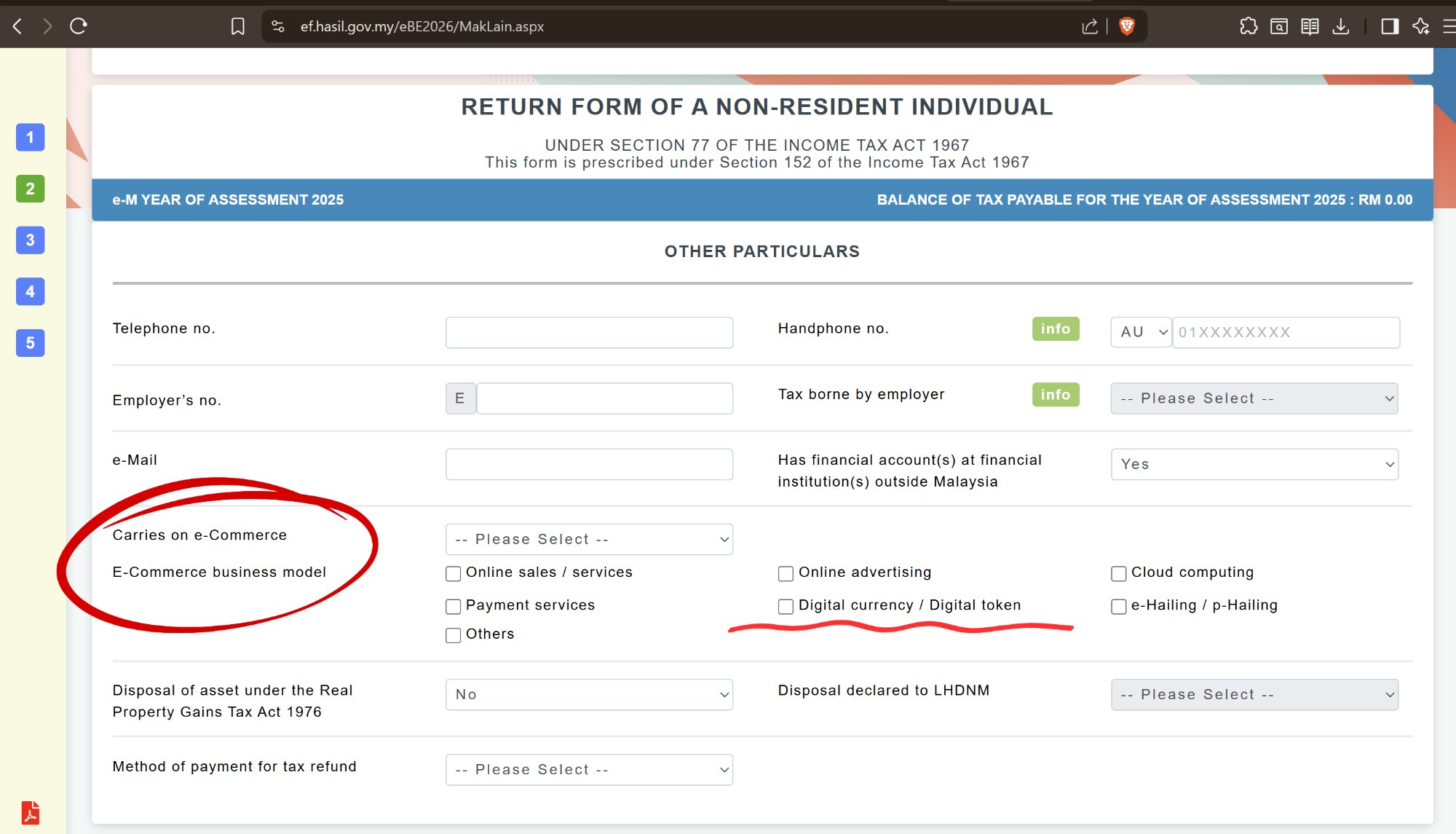

Non-resident form: Form M

Resident form: Form BE (no business) or Form B (business)

A Risk-Management Strategy

Why you may consider filing anyway

The case for voluntary filing rests on limitation periods and evidentiary positioning.

s.90(1) → File a return → deemed assessment on date of filing

s.91(1) → LHDN has 5 years from end of YA to raise additional assessments

s.90(3) → No return filed → DG may assess by best judgment

No time limit on this power

Filed vs Unfiled

What changes when you file?

Nil return filed

Deemed assessment created. Five-year limitation clock starts. Your position is documented at the time you formed it. Defensible if queried later.

No return filed

No deemed assessment. No clock running. The Director General can assess you by best judgment at any time. Your position has to be argued after the fact.

- Have you checked the Hasil Tax Portal to see if there are returns LHDN expects you to lodge?

- Does a nil return assert your position, or does not filing leave you exposed?

- Can you explain and defend your position if asked?

Note: s.91(3) removes all time limits in cases of fraud, wilful default, or negligence regardless of filing.

The Objection

"Doesn't filing put me in the tax net?"

No. Filing a nil return asserts a position. It does not concede chargeability.

A return completed with zeros across all income fields says: I was present in Malaysia, I assessed my position, and I concluded I have no Malaysian-source income and no tax liability.

That is a statement of facts and legal analysis, not an admission of jurisdiction. It does not create an obligation where none existed.

Practical Considerations

Visa holders and visibility

If you hold a visa tied to income thresholds, LHDN already knows you earn money.

- DE Rantau and similar visas require you to declare income to qualify. LHDN and immigration share data.

- A person known to authorities as an income-earning foreign national who has never lodged a return is in a weaker position than one who has filed a nil position.

- A clean filing history removes a line of enquiry before it starts, especially when renewing a visa or if your profile grows in Malaysia.

A Personal Bet

Don't be the low-hanging fruit

If you're here on a nomad visa, you're expected to file.

My personal bet is that failing to file at all will make me low-hanging fruit. And if there's a lot of low-hanging fruit around me and they come to harvest, I'm making sure that I don't get picked.

File. State your position. Start the clock. Be the green fruit up high.

Nil Filing Strategy

When your Malaysian tax outcome is nil

This applies where you have no Malaysian-source chargeable income, or where after claiming allowable deductions your net chargeable income in Malaysia is nil.

| Non-Resident (Form M) | Resident (Form BE / B) |

|---|

| Filing obligation on nil income | No on strict reading of s.77 | Arguable but LHDN expects filing |

| Effect of filing a nil return | Deemed assessment at nil; starts 5-year limitation clock under s.91 | Same mechanism applies |

| Effect of not filing | No clock. Open to best-judgment assessment under s.90(3), no time limit | Same risk applies |

| Recommended strategy | File voluntarily | File |

The limitation clock starts when you lodge. If your chargeable income is genuinely nil, filing protects that position.

Next Steps

When and how to file

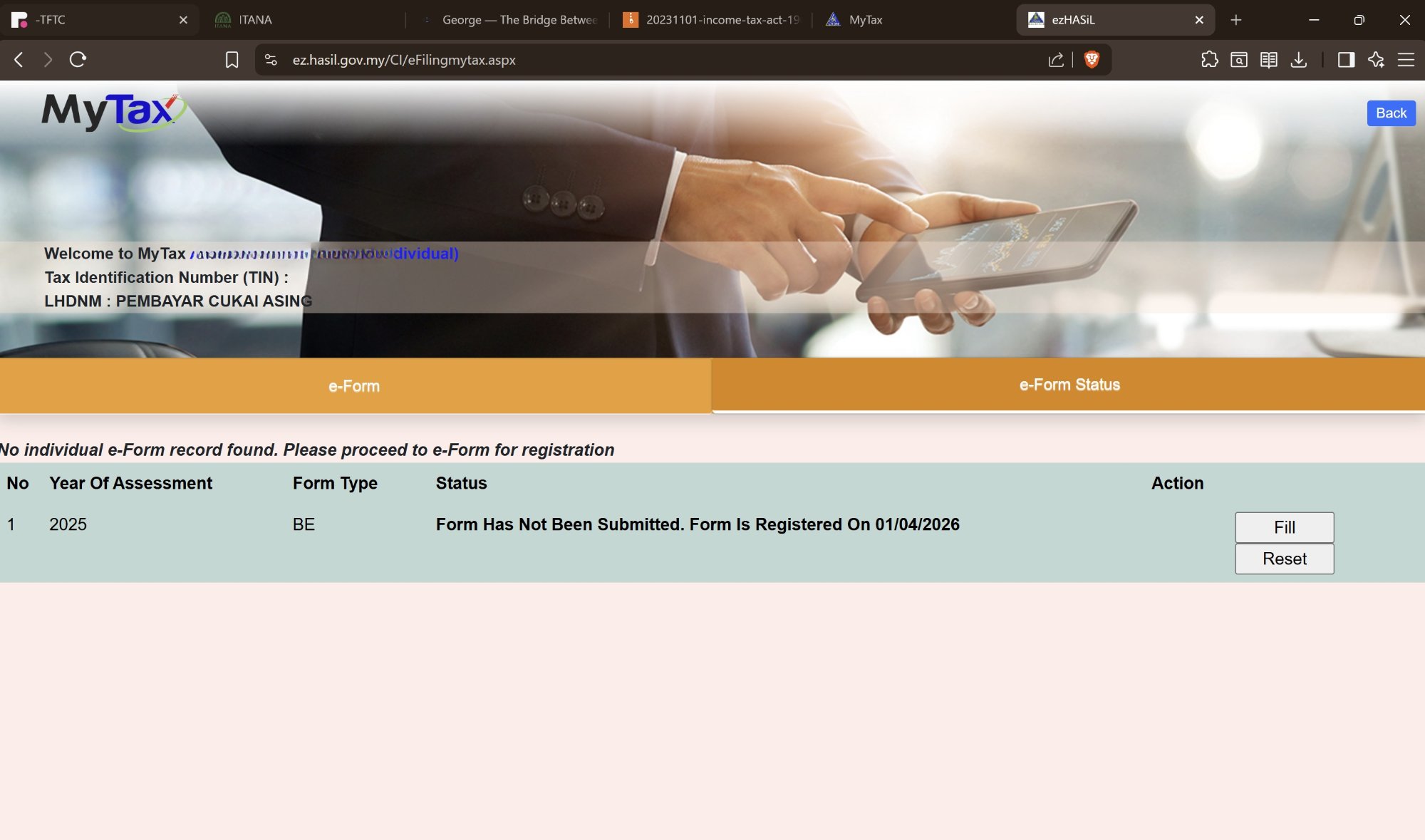

YA 2024 (Form M / BE) — due 30 April 2025 (overdue — file now)

YA 2025 (Form M / BE) — due 30 April 2026 (file by 15 May for e-filing)

YA 2025 (Form B) — due 30 June 2026 (file by 15 July for e-filing)

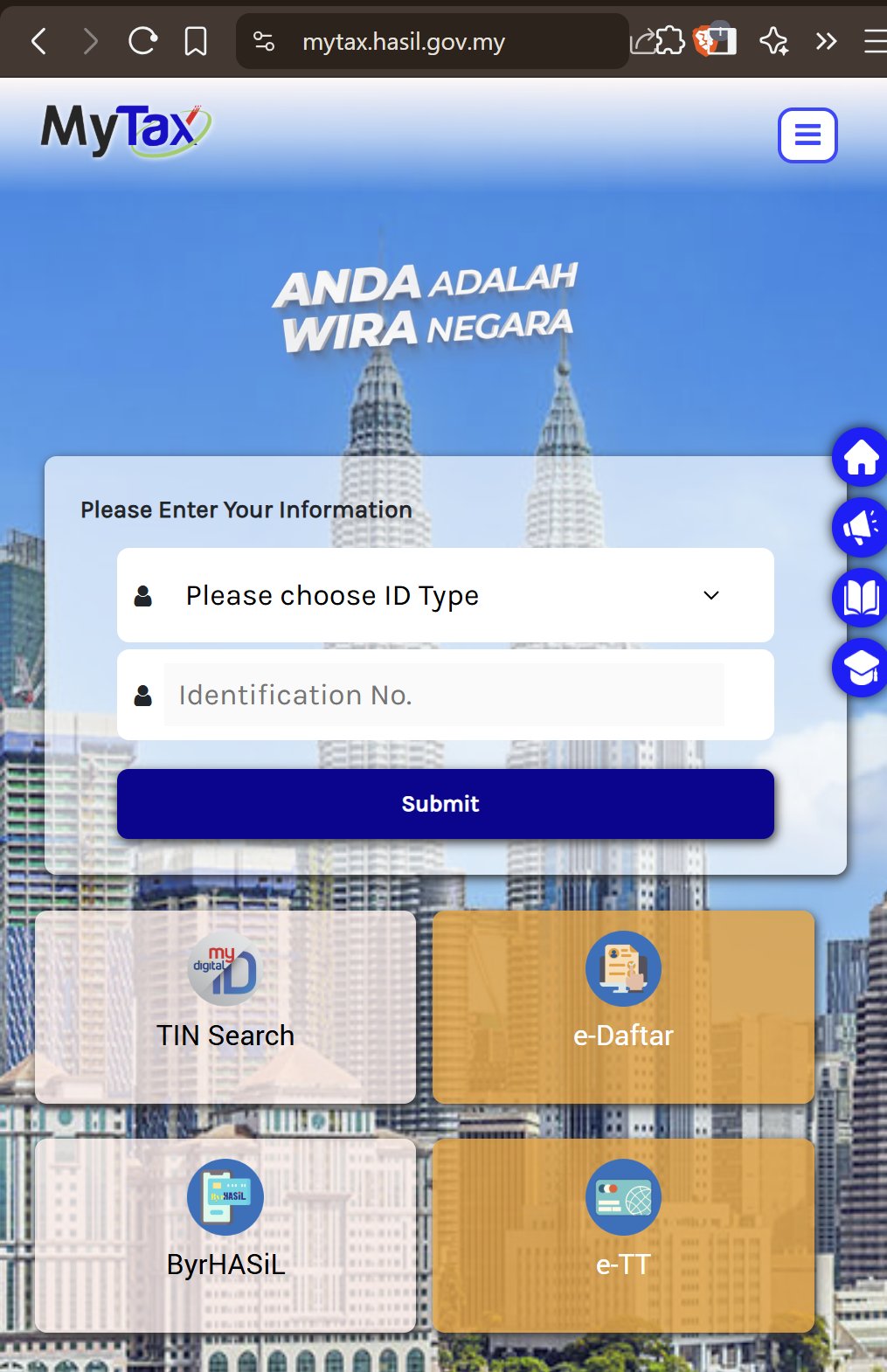

- Set up a login: Go to mytax.hasil.gov.my and register using your passport number.

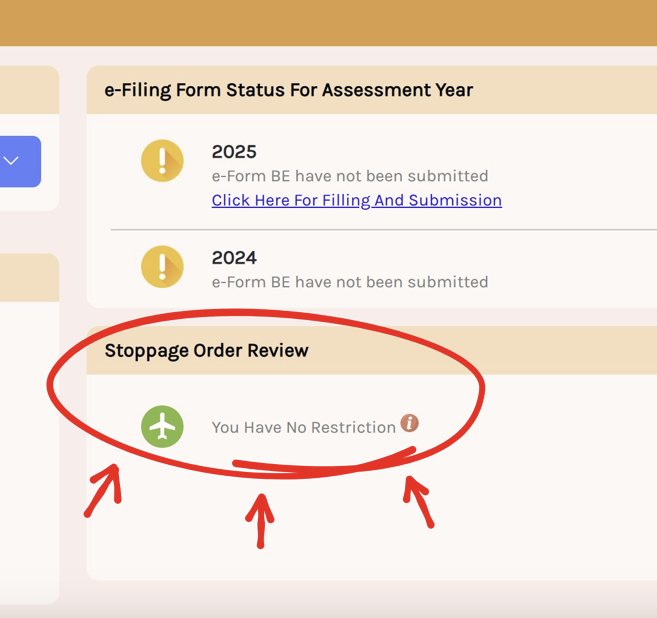

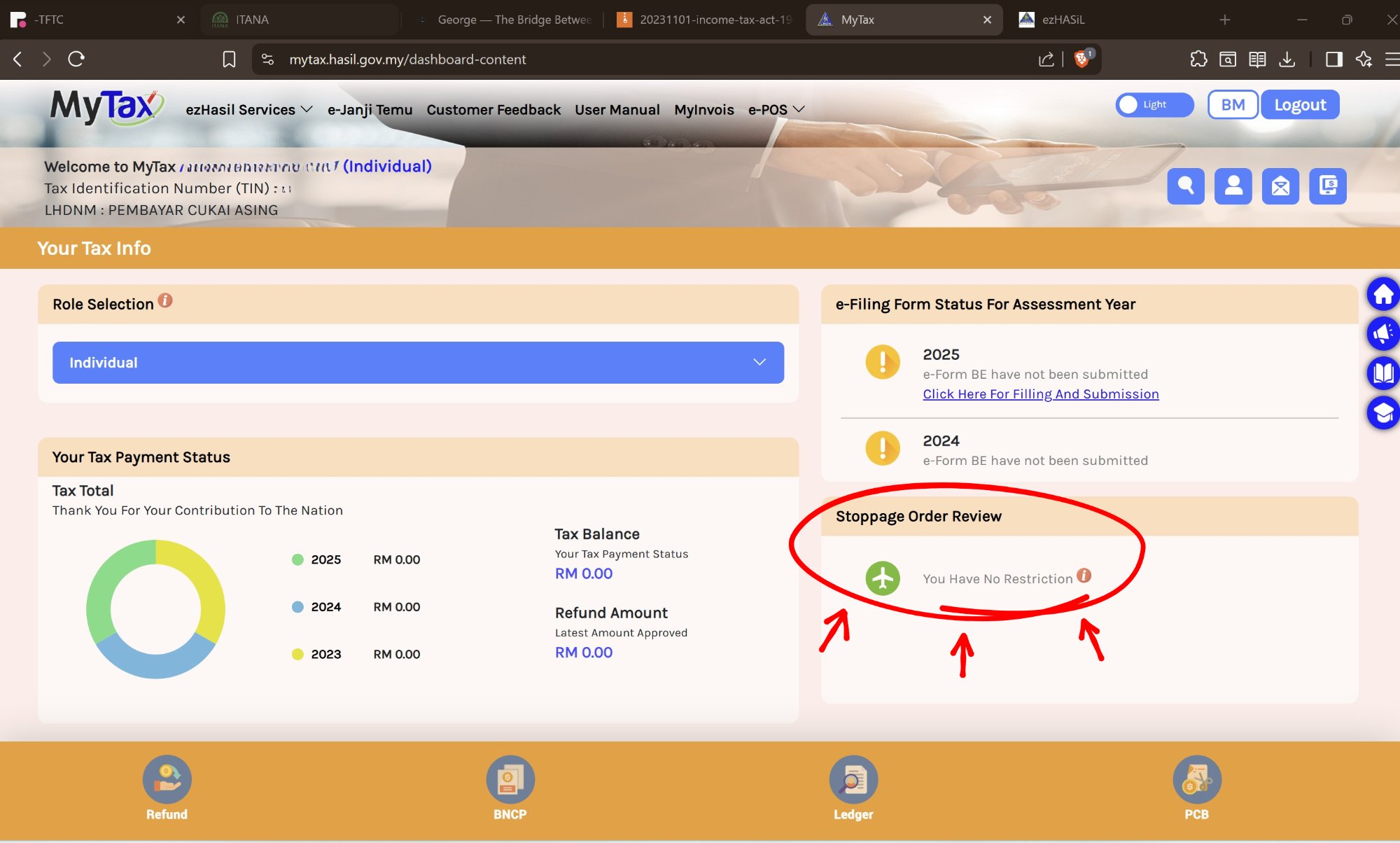

- Check your portal: If you applied for a DE Rantau visa you will have a tax ID number. Log in and you will see the returns LHDN expects you to lodge, and a small aeroplane icon indicating whether any movement restrictions have been placed on your file.

- Use a licensed Malaysian tax agent: they carry professional indemnity insurance and act as your representative with LHDN if anything goes wrong. Worth paying for.

- Late nil returns: the penalty is 10% of tax payable — on a nil return, that is zero. You are demonstrating good faith by filing voluntarily.

If You Get It Wrong

You can amend

Section 77B of the ITA allows one self-amendment per year of assessment.

- Submit an Amended Return Form (ARF) within six months of the original filing due date.

- If the amendment results in additional tax, a 10% increase applies on the additional amount.

- One amendment only. No ARF if LHDN has already raised an additional assessment under s.91.

- Outside the six-month window, you can still make a voluntary disclosure by letter to the LHDN office handling your file, with supporting documentation.

Get it right the first time if you can. But if your position changes or you discover an error, the system does allow correction.

A Note From Me

What I Do

- I am not a licensed Malaysian tax agent. I cannot give you advice or file your return.

- 20+ years in Australian public practice. Sold my practices. I now operate at the institutional level and build systems.

- I advise other accountants on international tax and crypto complexity for their clients. I have been automating this for 15 years because it's too hard and too expensive to manage manually.

- Asking me to do your tax is like asking the health system architect to write your prescription. Instead, let me build you the clinic.

- If you want more help with this, ask Network School to give me a space and support.

Find my sessions and office hours

lu.ma/electrafrost

I'm contributing this pro bono because I want Network School to retain its long-termers and be a success.

General information only. Not advice specific to individual circumstances. Confirm with the current text of the ITA 1967 and applicable LHDN public rulings and guidelines — or consult with a licensed tax agent.